we protect the employer.

Only Workride’s legal structure ensures employers can safely offer the benefit while fully recouping costs before ride ownership is offered to employees eliminating employer and director risks as a service provider. Check out the other options below and see why Workride has earned the trust by almost 2,000 organisations across New Zealand.

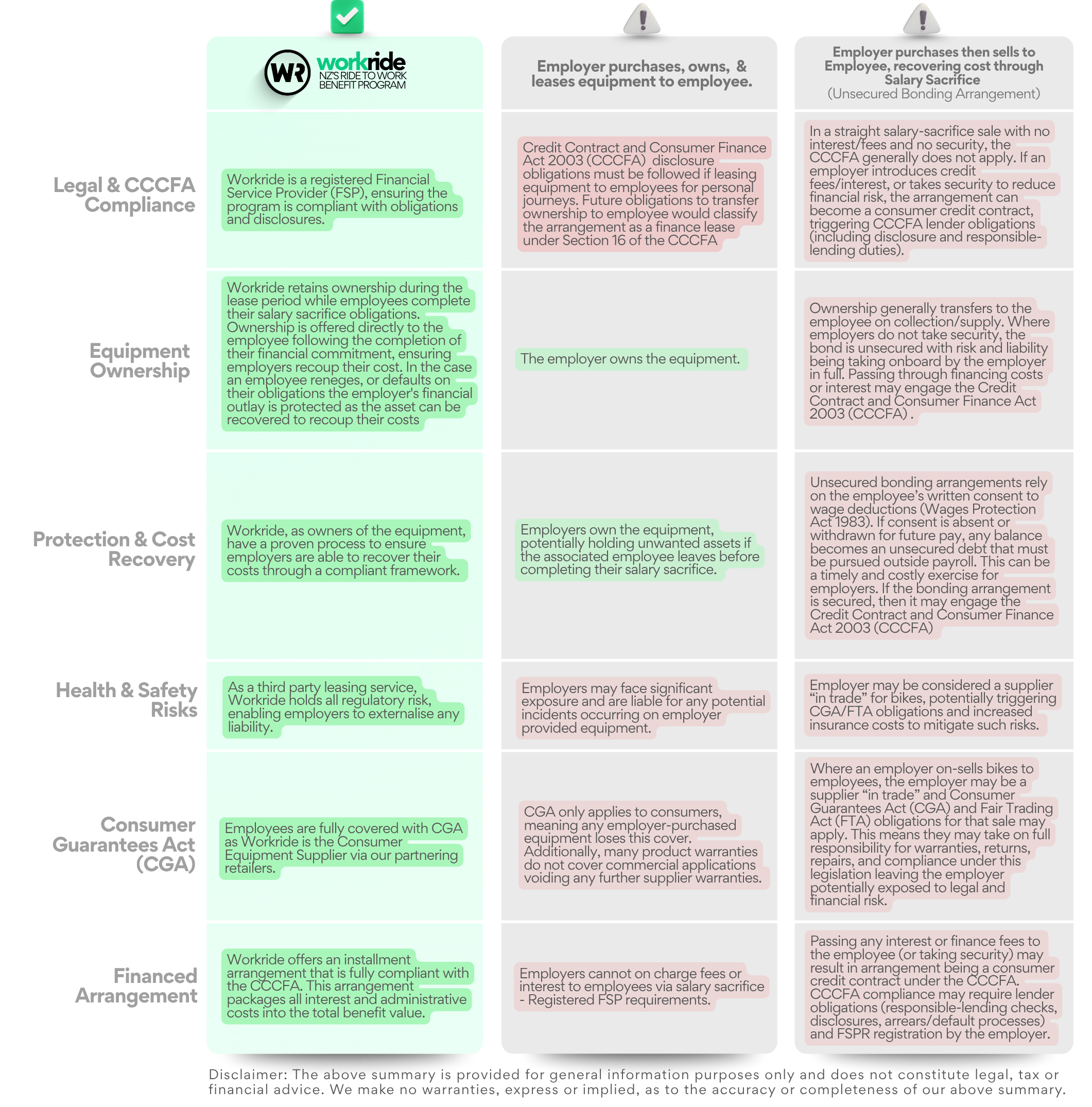

Workride – Fully Compliant & Protected Model

Legal & CCCFA Compliance

Workride is a registered Financial Service Provider (FSP), ensuring the program is compliant with obligations and disclosures.

Equipment Ownership

Workride retains ownership during the lease period while employees complete their salary sacrifice obligations. Ownership is offered directly to the employee following the completion of their financial commitment, ensuring employers recoup their cost. In the case an employee reneges, or defaults on their obligations the employer's financial outlay is protected as the asset can be recovered to recoup their costs

Protection & Cost Recovery

Workride, as owners of the equipment, have a proven process to ensure employers are able to recover their costs through a compliant framework.

Health & Safety Risks

As a third party leasing service, Workride holds all regulatory risk, enabling employers to externalise any liability.

Consumer Guarantees Act (CGA)

Employees are fully covered with CGA as Workride is the Consumer Equipment Supplier via our partnering retailers.

Financed Arrangement

Workride offers an installment arrangement that is fully compliant with the CCCFA. This arrangement packages all interest and administrative costs into the total benefit value.

Employer Owns & Leases Equipment to Employee

Legal & CCCFA Compliance

Credit Contract and Consumer Finance Act 2003 (CCCFA) disclosure obligations must be followed if leasing equipment to employees for personal journeys. Future obligations to transfer ownership to employee would classify the arrangement as a finance lease under Section 16 of the CCCFA

Equipment Ownership

The employer owns the equipment.

Protection & Cost Recovery

Employers own the equipment, potentially holding unwanted assets if the associated employee leaves before completing their salary sacrifice.

Health & Safety Risks

Employers may face significant exposure and are liable for any potential incidents occurring on employer provided equipment.

Consumer Guarantees Act (CGA)

CGA only applies to consumers, meaning any employer-purchased equipment loses this cover. Additionally, many product warranties do not cover commercial applications voiding any further supplier warranties.

Financed Arrangement

Employers cannot on charge fees or interest to employees via salary sacrifice - Registered FSP requirements.

Employer purchases then sells to Employee, recovering cost through Salary Sacrifice (Unsecured Bonding Arrangement)

Legal & CCCFA Compliance

In a straight salary-sacrifice sale with no interest/fees and no security, the CCCFA generally does not apply. If an employer introduces credit fees/interest, or takes security to reduce financial risk, the arrangement can become a consumer credit contract, triggering CCCFA lender obligations (including disclosure and responsible-lending duties).

Equipment Ownership

Ownership generally transfers to the employee on collection/supply. Where employers do not take security, the bond is unsecured with risk and liability being taking onboard by the employer in full. Passing through financing costs or interest may engage the Credit Contract and Consumer Finance Act 2003 (CCCFA) .

Protection & Cost Recovery

Unsecured bonding arrangements rely on the employee’s written consent to wage deductions (Wages Protection Act 1983). If consent is absent or withdrawn for future pay, any balance becomes an unsecured debt that must be pursued outside payroll. This can be a timely and costly exercise for employers. If the bonding arrangement is secured, then it may engage the Credit Contract and Consumer Finance Act 2003 (CCCFA)

Health & Safety Risks

Employer may be considered a supplier “in trade” for bikes, potentially triggering CGA/FTA obligations and increased insurance costs to mitigate such risks.

Consumer Guarantees Act (CGA)

Where an employer on-sells bikes to employees, the employer may be a supplier “in trade” and Consumer Guarantees Act (CGA) and Fair Trading Act (FTA) obligations for that sale may apply. This means they may take on full responsibility for warranties, returns, repairs, and compliance under this legislation leaving the employer potentially exposed to legal and financial risk.

Financed Arrangement

Passing any interest or finance fees to the employee (or taking security) may result in arrangement being a consumer credit contract under the CCCFA. CCCFA compliance may require lender obligations (responsible-lending checks, disclosures, arrears/default processes) and FSPR registration by the employer.

Disclaimer: The above summaries is provided for general information purposes only and does not constitute legal, tax or financial advice. We make no warranties, express or implied, as to the accuracy or completeness of our above summary.